Positioned for fundamentals, not sentiment

In brief

Markets are rewarding short‑term defensiveness in some areas and punishing quality elsewhere. We unpack what’s being left out, where sentiment has overshot fundamentals, and how our active, ethical approach is uncovering opportunity in a highly dispersed market.

Oil supply shocks, persistent inflation, constrained central banks and accelerating AI disruption have converged at the same time. The result has been heightened volatility across both equities and bonds.

While markets have repriced quickly, the underlying fundamentals of many businesses remain resilient, and in some cases, our valuations are much higher than company share prices. For advisers, this environment raises questions about portfolio positioning and what lies ahead. At Australian Ethical, our decisions continue to be guided by fundamentals, valuation and long-term themes – not short-term headlines.

Discomfort, dispersion and opportunity

The Australian equity market has felt unsettled.

Leadership has narrowed, with Materials, Energy outperforming, while 72% of ASX200 stocks ended the quarter lower. Sector rotation that began in 2025 continued into early 2026, with Materials outperforming Industrials by around 10%.

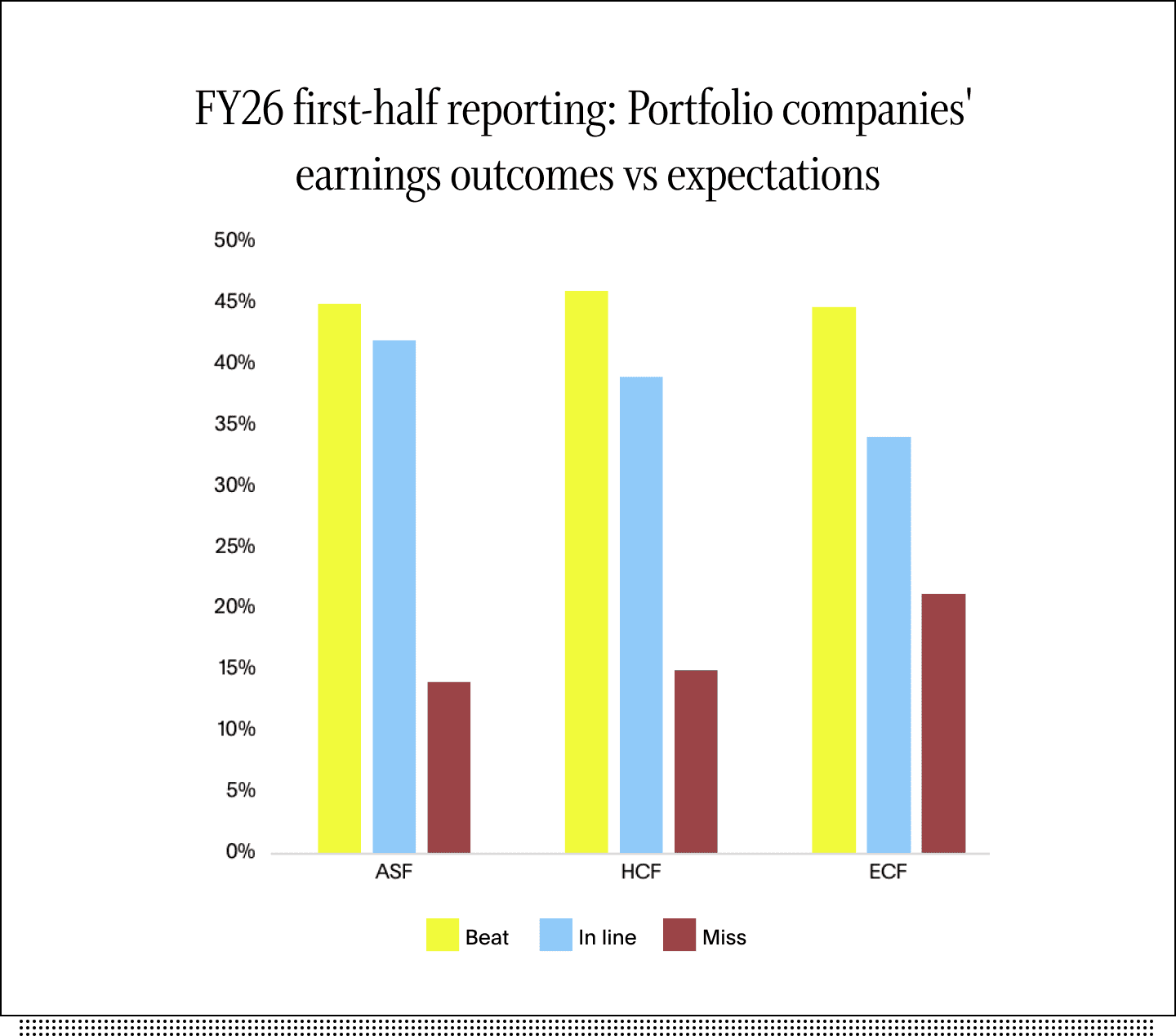

Importantly, price action has moved faster than fundamentals. Reporting season showed that around 80% of companies held across our portfolios met or exceeded earnings expectations. Dispersion across sectors and stocks remains high, which increases the opportunity set for selective positioning rather than broad market exposure.

Importantly, price action has moved faster than fundamentals. Reporting season showed that around 80% of companies held across our portfolios met or exceeded earnings expectations. Dispersion across sectors and stocks remains high, which increases the opportunity set for selective positioning rather than broad market exposure.

Source: Australian Ethical Investment, April 2026

Sentiment has outpaced fundamentals, particularly in software

The selloff in software and technology stocks illustrates a growing disconnect between sentiment and fundamentals. Market concern about AI disruption has driven broad, indiscriminate selling, often ignoring earnings growth, balance sheet strength and business model resilience.

This has meant that weaker business models have been sold down alongside companies that are actively strengthening their competitive positioning through AI. In that context we believe the selloff has potentially obscured important differences in how businesses are adapting in the way they are deploying capital and talent.

The SiteMinder example

The ASX-listed hotel software provider was heavily sold down during the AI-led disruption concerns.

SiteMinder sits at the centre of hotel operations, helping properties manage reservations and pricing across all channels of distribution – or how hotel rooms are sold. This is a workflow where speed, accuracy and reliability matter. Errors can result in disrupted travel plans for guests and lost revenue and or reputation for businesses. As the platform scales, its role in distribution becomes increasingly important.

Recent market moves have often grouped businesses like SiteMinder with more vulnerable software models. Yet the company is using AI to improve their core processes – strengthening execution and decision making rather than displacing its position. In this case, short, sharp selloffs temporarily obscured the difference between sentiment and business fundamentals in our view.

Our conviction is grounded in detailed fundamental work and an awareness of how valuation shifts can create opportunity. This is also evident in businesses such as Xero and PEXA.

Active decisions, not passive endurance

At the same time, repricing – short and sharp as it may be at times – has pushed valuations in some areas to historically low multiples improving the starting point for active investors with a longer-term view like us.

During the quarter, we deployed capital into areas of weakness rather than waiting for clearer headlines. Cash levels across portfolios are now less than 1%, the lowest in years. This reflects our assessment that current valuations in select parts of the market are attractive, even though volatility is likely to persist. Our conviction is grounded in detailed fundamental work and an awareness of how valuation shifts can create opportunity.

This approach is informed by experience across multiple market cycles.

Ethical discipline and system resilience

Our ethical approach shapes how we think about risk – particularly system level risk.

Recent geopolitical shocks again highlighted the global economy’s exposure to fossil fuel‑based energy systems. While some funds may benefit in the short term from oil, gas or cyclical resource exposure, history suggests these gains are often followed by weaker forward returns.

We deliberately restrict investments in companies that extract, sell or distribute fossil fuels, and in some of the largest consumers of oil and gas. This can help limit sensitivity to rising energy prices and aligns capital with businesses addressing durable, real‑world needs, including healthcare, digital infrastructure, essential services and the transition to a lower‑carbon economy. These are the areas our portfolios are naturally skewed.

At times, this means our portfolios won’t track the broader market. When excluded or underweight sectors rise quickly, relative performance may lag. That doesn’t signal a broken process. It is the result of a disciplined investment process designed to deliver differentiated outcomes from broader-market investors.

Valuation discipline in action

Recent positioning decisions reflect that discipline. Banks have benefited from risk‑off sentiment, with valuations now well above long‑term averages. We’ve actively trimmed positions, including Westpac, reallocating capital toward areas where valuations better reflect underlying risk and long‑term growth potential.

Short‑term defensiveness can feel reassuring. Elevated multiples, however, reduce long‑term return appeal.

Staying the course is an active choice

Short‑term performance often reflects where markets are in their cycle, not whether an investment approach is sound. Over time, outcomes are driven by consistency, valuation discipline and exposure to enduring structural trends — such as digitalisation, ageing populations and the transition to a lower‑carbon economy.

In this environment, staying the course isn’t passive. It’s an active decision to prioritise fundamentals over sentiment, and long-term outcomes over short-term noise.

Get in touch

If you would like to find out more, fill in your details below and our Business Development team will be in touch.

Interests in the Australian Ethical Managed Funds are issued by Australian Ethical Investment Ltd (ABN 47 003 188 930, AFSL 229949), the Responsible Entity of the Australian Ethical Managed Funds.

This article has been prepared for use by advisers only. It must not be made available to any client and any information in it must not be communicated to any client.

This information is of a general nature and is not intended to provide you (or your clients) with financial advice or take into account your (or your clients’) personal objectives, financial situation or needs. Before acting on the information, consider its appropriateness to your circumstances and read the product disclosure statement (PDS), information memorandum and target market determination (TMD) for the relevant product and the financial services guide available on our website.

Australian Ethical Investment Ltd does not guarantee the performance of any fund or the return of an investor’s capital; past performance is not a reliable indicator of future performance.

Certain statements in this article relate to the future. Such statements involve known and unknown risks and uncertainties and other important factors that could cause the actual results, performance or achievements to be materially different from expected future results. Australian Ethical Investment Ltd does not give any representation, assurance or guarantee that the events expressed or implied in any forward looking statements in this update will actually occur and you are cautioned not to place undue reliance on such statements.

This article may contain material provided by third parties derived from sources believed to be accurate at its issue date. While such material is published with necessary permission, the Australian Ethical Investment Ltd accepts no responsibility for the accuracy or completeness of, nor does it endorse any such third party material. To the maximum extent permitted by law, we intend by this notice to exclude liability for this third party material.

Investing ethically and sustainably means that the investment universe will generally be more limited than non-ethical, non-sustainable portfolios in similar asset classes. This means that the portfolio(s) may not have exposure to specific assets which over or underperform over the investment cycle, and so the returns and volatility of the portfolio(s) may be higher or lower than non-ethical, non-sustainable portfolios over all investment time frames.