What your portfolio is built for

In brief

How portfolios are built matters. This article explains how our approach shapes capital allocation and risk by focusing on how the economy is changing, resulting in portfolios designed to support long-term growth and real-world outcomes.

Your decision to invest with Australian Ethical might start with values. But it extends to something more practical: how your money is positioned to grow as the world changes. This is what our portfolios are built for.

Designed for where growth is heading

Ethical investing is sometimes misunderstood as a set of exclusions. In practice, it’s much closer to a long‑term allocation to where growth is likely to come from.

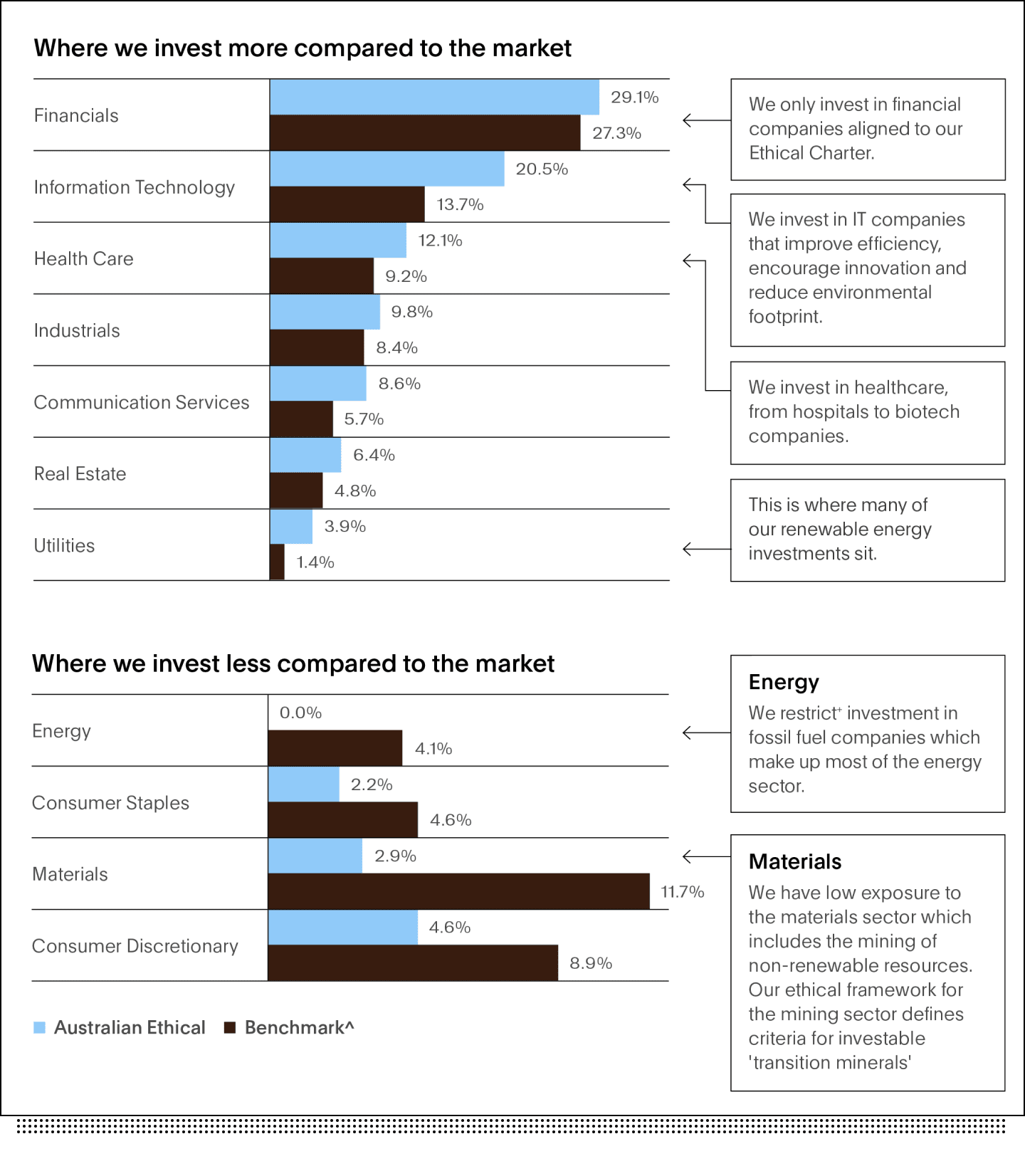

Our portfolios at Australian Ethical don’t simply mirror the share market. They are deliberately tilted toward businesses solving real‑world problems and operating in parts of the economy with durable demand. That includes areas like clean energy, healthcare, digital infrastructure and essential services – industries shaped by long‑term forces rather than the short‑term cadence of investment cycles.

* Compared to a blended share market Benchmark of S&P ASX200 Index (for Australian and NZ shareholdings) and MSCI World ex Australia Index (for international shareholdings). For the purpose of this sector analysis, GREIT exposures within our Property strategy have been excluded from portfolio .

^ Compared to a blended benchmark that best reflects the benchmarks used by the underlying investment strategies. Based on holdings at 30 June 2025 and analysis tools provided by external sources which cover ~74% of the investments we hold by value other than wholesale cash fund and mandates. Both carbon intensity and sustainable impact solutions revenue relate to the listed companies and public corporate fixed income securities in which we invest across our funds and options. This should not be considered representative of individual funds or options which will have their own mix of share and other investments.

+ Our investment restrictions include some thresholds. Thresholds may be in the form of an amount of revenue that a business derives from a particular activity, but there are other tolerance thresholds we can use depending on the nature of the investment. We apply a range of qualitative and quantitative analysis to the way we apply thresholds. For example, we may make an investment where we assess that the positive aspects of the investment outweigh its negative aspects. For information on how we make these assessments for a range of investment sectors and issues such as fossil fuels, nuclear power, gambling, tobacco, human rights, and many others, please read our Ethical Guide.

There’s a reason our portfolios are built this way. Take healthcare: Ageing populations, intrinsic demand and the need for continuous innovation and advancement across biotech, medical devices and digital health create conditions for long‑term growth.

Or technology: digitalisation isn’t a fad, it’s an ongoing shift, with businesses across every industry moving toward software, automation, data and AI to improve efficiency and decision-making.

These aren't just short term themes. They are parts of the economy with characteristics we believe support durable growth over time. Each with important economic characteristics: scalable business models, recurring revenues, intellectual property and the ability to grow without needing ever-increasing amounts of capital.

We think these are important characteristics that matter, not just to investors, but also for people, planet and animals.

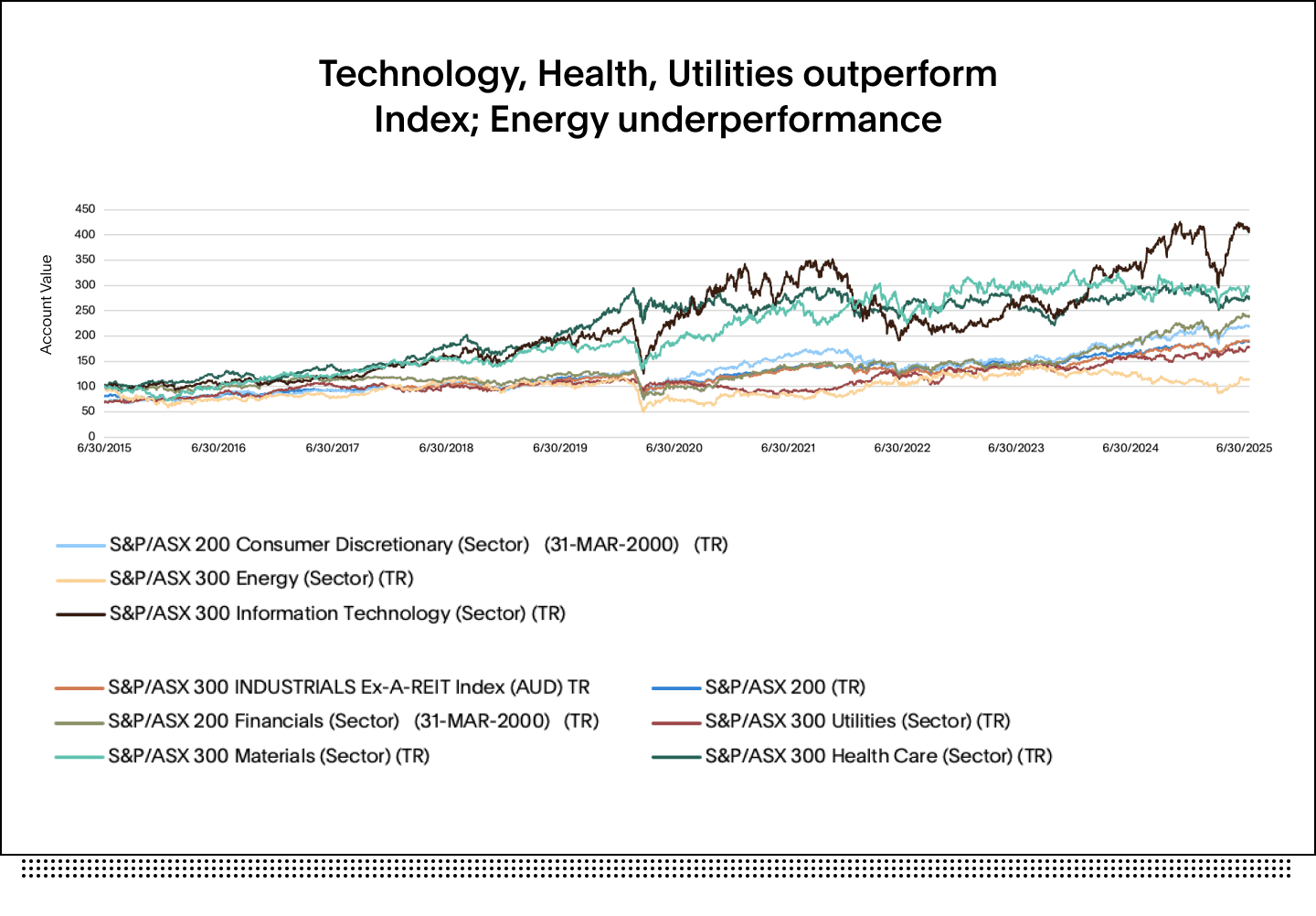

At times, the areas our Ethical Charter steers us towards or away from will perform differently to the broader market. For example, in the second half of 2025, materials stocks – including miners – outperformed. Because we don’t invest in many of these companies, our portfolios delivered different results to mainstream funds and benchmarks.

Our portfolios are intentionally positioned differently from the broader market, so performance will vary at times. But across multiple timeframes, many of the sectors consistently favoured under our Ethical Charter have also been among the strongest performers, while those we’re remained underweight have lagged (see chart below). This reflects a deliberate emphasis on long-term structural growth rather than short-term market trends.

Built to connect your money with real outcomes

Markets often talk in abstractions: sectors, indices, benchmarks, asset classes. But your money ultimately flows into real businesses, projects and services that shape how the world works.

While we map our investments to financial benchmarks and express our portfolio weightings by sector and asset classes, we also measure our investments against real-world outcomes, including the UN Sustainable Development Goals. This is not used as a badge or slogan, but as a way of showing where capital is actually being directed, independent of financial markets definitions.

Using these measures, our portfolios generate significantly higher revenue exposure to sustainable solutions from clean energy and energy efficiency to water, agriculture, education and digital connectivity than mainstream funds and benchmarks1. These aren’t side projects, they’re areas of growing economic relevance.

Consider aged care: as Australia’s population ages, demand for quality care is increasing, especially in regional areas. Through our investment in For Purpose Aged Care Australia, capital supports the expansion of not-for-profit aged care homes delivering services where they’re most needed, while generating a financial return.

Or infrastructure: through our Infrastructure Debt Fund, we provide financing for renewable energy projects and social infrastructure like schools, hospitals and social housing. In its first year, the fund delivered returns while supporting renewable energy for the equivalent of hundreds of thousands of homes.

One example is Octopus Energy, which approaches the energy transition as a system – combining renewable generation, smart technology and household energy management so cleaner power is reliable and easier to use. It’s a reminder that long‑term value is often built where technology, infrastructure and everyday needs intersect.

Built to manage risks you don’t always see

Not all risks show up immediately in share market prices. Some risks sit in business models that depend on finite resources, rising environmental costs or increasingly complex regulation. Others appear in poor governance, weak oversight or social and environmental impacts that eventually become financial liabilities. This is why ethical investing is, at its core, a form of risk management.

Take materials. This part of the market can generate strong returns at times, but it’s capital‑intensive, cyclical, and constrained by geology and regulation. Growth typically requires ever‑greater capital, often with diminishing returns and rising risk of assets being stranded. That creates a different risk and return profile to sectors like technology and healthcare, where growth can often scale with less physical capital.

Environmental and social risks are investment risks, with negative impacts often surfacing later through regulation, litigation or loss of trust. Alongside governance, these considerations inform our ethical process, which seeks to direct capital toward positive outcomes and manage risks relevant to long‑term value.

Diversification plays a role too. Our portfolios offer a different breadth of exposure by design, with allocations shaped by ethics, valuation and long-term trends rather than market weight alone. That is designed to help build resilience when markets are unsettled.

Future focused investments

Ethical investing isn’t about trying to predict the next quarter. It’s about deciding what your money is built for.

If you chose ethical investing, you likely did so because you wanted your capital aligned with the world you see emerging – not just the one that exists today. That decision remains a disciplined way of navigating risk, opportunity and long‑term value.

In this way, ethical investing connects capital with outcomes, not by sacrificing returns, but by aligning them with where demand and investment are heading.

1. Overall, revenue from sustainable impact solutions is 2.3 times the sustainable impact revenue for an equivalent investment in the Benchmark. Revenue from sustainable water and agriculture and pollution prevention solutions is 5.2 times Benchmark. On the climate front, revenue from Alternative Energy is 2.7 times, Green Building 2.5 times and Energy Efficiency is 1.8 times that of the Benchmark. In terms of human flourishing, our investments in Education are 3.0 times that of the Benchmark and in Connectivity (an enabler of social interaction and efficiency) we are 13.5 times the Benchmark. Carbon intensity (tonnes CO₂-e /$ revenue), sustainable impact solutions revenue, and investment in renewables and energy solutions measures all relate to our investment in listed shares and public corporate fixed income securities across our funds and options for which we have relevant data. This should not be considered representative of individual funds or options which will have their own mix of share and other investments. We report on our investments in listed shares and fixed income securities because these comprise a large proportion of our total funds under management (~81.0%), and because data is less readily available across our other investments.

If you chose ethical investing, you likely did so because you wanted your capital aligned with the world you see emerging – not just the one that exists today. That decision remains a disciplined way of navigating risk, opportunity and long term value.

In this way, ethical investing connects capital with outcomes, not by sacrificing returns, but by aligning them with where demand and investment are heading.

Interests in the Australian Ethical Managed Funds are issued by Australian Ethical Investment Ltd (ABN 47 003 188 930, AFSL 229949), the Responsible Entity of the Australian Ethical Managed Funds.

This communication has been prepared for use by advisers only. It must not be made available to any client and any information in it must not be communicated to any client. This information is of a general nature and is not intended to provide you (or your clients) with financial advice or take into account your (or your clients’) personal objectives, financial situation or needs. Before acting on the information, consider its appropriateness to your circumstances and read the product disclosure statement (PDS), information memorandum and target market determination (TMD) for the relevant product and the financial services guide available on our website.

Australian Ethical Investment Ltd does not guarantee the performance of any fund or the return of an investor’s capital; past performance is not a reliable indicator of future performance.

Certain statements in this communication relate to the future. Such statements involve known and unknown risks and uncertainties and other important factors that could cause the actual results, performance or achievements to be materially different from expected future results. Australian Ethical Investment Ltd does not give any representation, assurance or guarantee that the events expressed or implied in any forward looking statements in this update will actually occur and you are cautioned not to place undue reliance on such statements.

This article may contain material provided by third parties derived from sources believed to be accurate at its issue date. While such material is published with necessary permission, the Australian Ethical Investment Ltd accepts no responsibility for the accuracy or completeness of, nor does it endorse any such third party material. To the maximum extent permitted by law, we intend by this notice to exclude liability for this third party material.

Investing ethically and sustainably means that the investment universe will generally be more limited than non-ethical, non-sustainable portfolios in similar asset classes. This means that the portfolio(s) may not have exposure to specific assets which over or underperform over the investment cycle, and so the returns and volatility of the portfolio(s) may be higher or lower than non-ethical, non-sustainable portfolios over all investment time frames.