Staying steady: Understanding your super’s long-term journey

In Brief

Short-term movements in your balance are expected and often don’t reflect the bigger picture. Understanding how super is designed and why long-term investing matters can help you stay on track, regardless of day-to-day changes.

This article guides you through the ups and downs of your super balance, showing why focusing on long-term growth is the key to staying confident and on track.

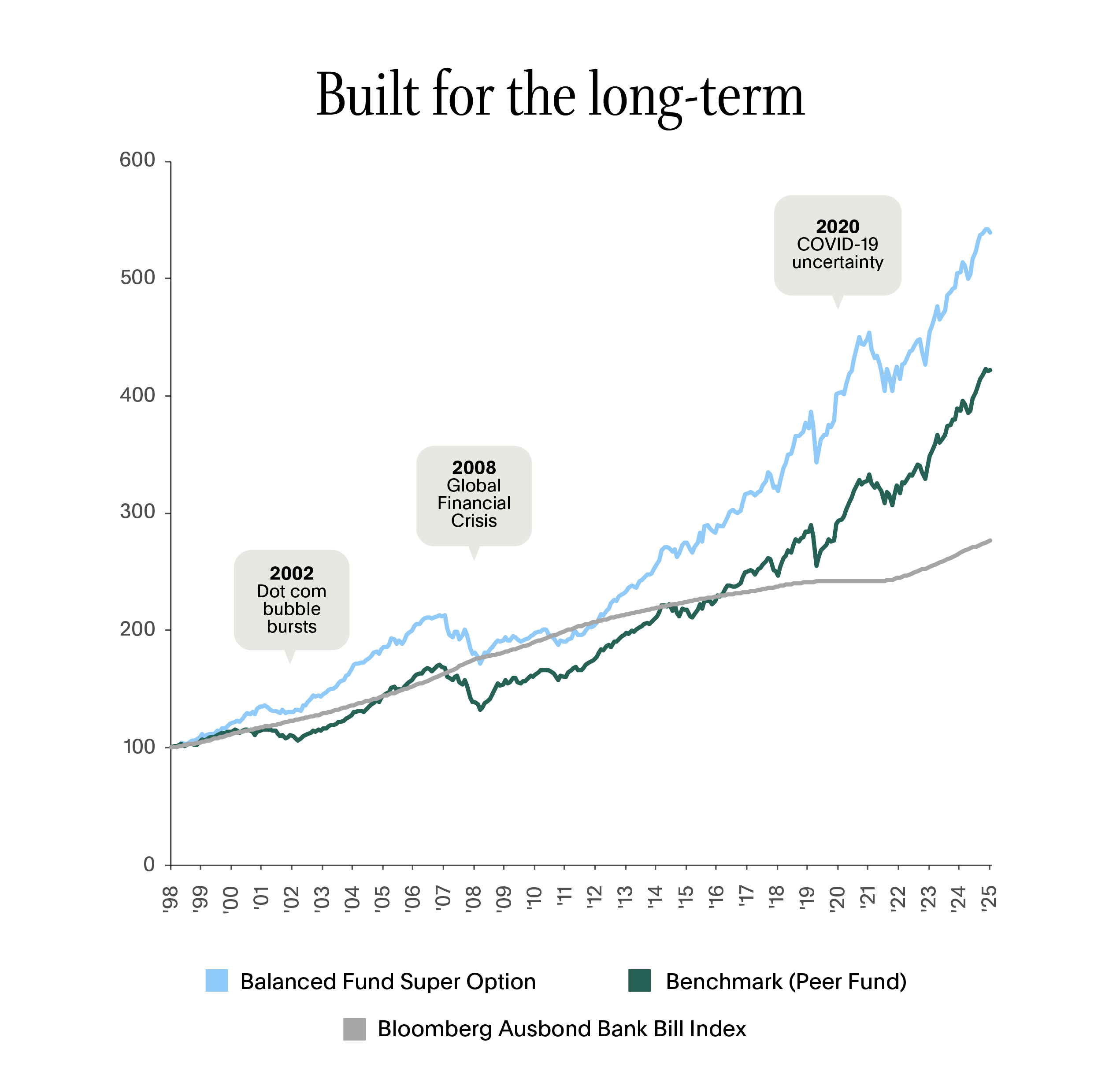

Super is built for the long term

Super is designed to support you across different stages of life – from growing your balance over time to providing income when you’re ready to retire. How your money is invested reflects that journey, with longer timeframes allowing greater exposure to assets that may fluctuate in the short term, and shorter timeframes placing more emphasis on stability and income.

Balanced Fund Super Option return is net of investment fees, admin fees and tax, gross of $-based member fee. Past performance is not a reliable indicator of future returns.

Peer fund benchmark was Morningstar Multisector Balanced - Superannuation index until Mar-2015, Morningstar Multisector Growth - Superannuation index until Dec-2019, SuperRatings SR50 Balanced (60-76) Index to current. Peer fund return is net of investment fees, admin fees and tax, gross of $-based member fee.

Volatility is uncomfortable – but it’s not unusual

Market volatility simply means prices moving up and down, and it happens as investors react to different pieces of news or events and try to interpret whether they’re positive or negative for the value of their investments. Your super is an investment, so its value can also go up and down as markets move.

Market volatility is normal and expected in investing, and you’ll likely experience many periods of volatility during the time your super is invested. Our ethical investment team is experienced at investing your super through all market conditions, with the aim of growing it for your retirement.

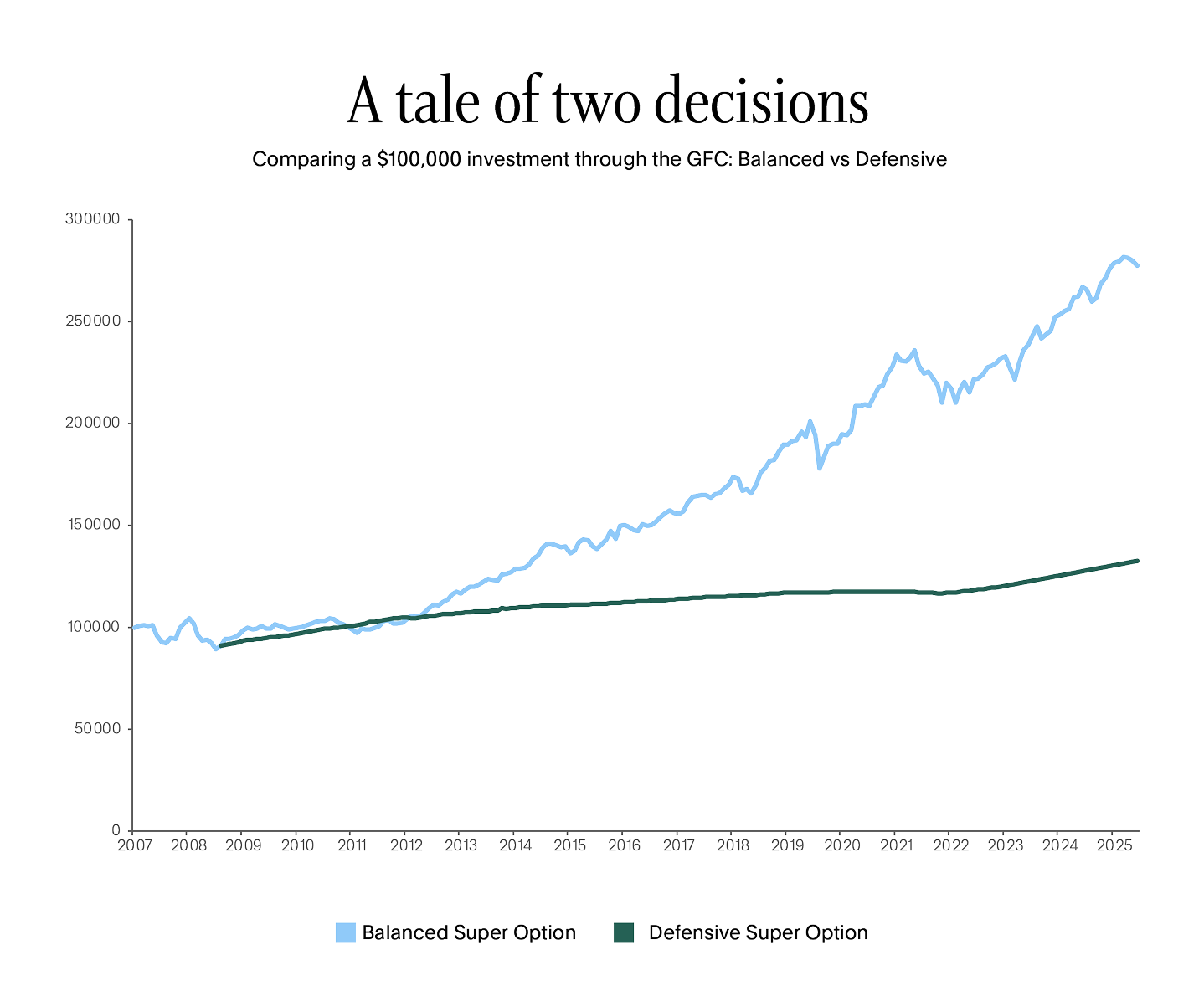

Why moving your money into lower risk options is not always a good idea

When balances fall, it can be tempting to move money into lower risk investment options to “stop the damage”. While these options may feel safer in the short term, they typically deliver lower returns over time. And switching after markets have fallen can mean:

- Locking in losses

- Missing out on potential recoveries

- Interrupting the long‑term compounding that helps grow your super

Net of investment fees, % based admin fee, tases. Gross of $-based member fee. Past performance is not an indication of future returns.

The quiet power of compounding

Compounding is the process where returns build on top of returns over time. It works best when money stays invested and time is allowed to do its work. Short term ups and downs don’t stop compounding, but stepping out of the market can interrupt it.

Staying invested through different market conditions gives your super the best chance to benefit from long‑term growth.

The importance of diversification

Your super isn’t invested in just one place. Most super investment options are diversified across a range of different asset classes– not only shares, but also assets like fixed income, property, infrastructure, and investments across different regions and industries. Because these assets don’t all move in the same way at the same time, your balance won’t always move in line with share markets.

Diversification can prevent ups and downs, but it helps reduce reliance on any single market outcome and smooth returns through different market conditions.

Staying focused on the long term

Long‑term investing isn’t about avoiding ups and downs. It’s about understanding them, expecting them , and not letting short‑term movements distract you from your long‑term goals.

By staying focused on why you invested in the first place, you give your super the best chance to do what it’s designed to do, which is to support your future.

This is general information only and does not take account of your individual investment objectives, financial situation or needs. Before acting on it, consider its appropriateness to your circumstances and read the Product Disclosure Statement (PDS), and Target Market Determination (TMD) available on our website. You should consider seeking advice from a licensed financial adviser before making an investment decision.